7 ways to bounce back your credit after overspending

Get a handle on debt with these simple steps.

Credit: Reviewed / Getty Images / vladwel / Nuthawut Somsuk

Credit: Reviewed / Getty Images / vladwel / Nuthawut Somsuk

Recommendations are independently chosen by Reviewed's editors. Purchases made through the links below may earn us and our publishing partners a commission.

It’s been a challenging couple of years for many Americans, and now there is the highest inflation to contend with in 40 years. If you turned to credit cards to get you through these tough financial times, your credit and your wallet might have taken a hit. If you’re ready to get out of debt, here are seven ways to bounce back your credit after overspending.

1. Understand credit utilization ratios

A good rule of thumb is to keep your credit card utilization under 30%.

A credit score determines how you manage or utilize your available credit limits. If you are close to or even over the limit with a credit card, this hurts your credit score. Maintaining low balances or paying off your card in full each month will keep your utilization low, which will positively affect your credit score.

“The reason overspending can harm your credit is because of the various "utilization" ratios considered by credit scoring systems, like FICO,” saysJohn Ulzheimer, a credit expert and author who formerly worked for FICO, Equifax, and Credit.com. “The most important is the revolving utilization ratio, which considers the balances on your credit cards relative to the credit limits on your credit cards.”

2. Target credit card debt

The simplest way that overspenders can improve their credit scores is by paying down credit card debt. Doing so will improve their revolving utilization ratio and boost their credit score. Paying off their balance will save them money by knocking down the interest charges on their credit card accounts. Achieving financial freedom afterpaying down credit card debtis its own reward.

“反弹超支后你的信用是really an exercise in paying down your credit card debt,” Ulzheimer says.”Spending a lot in the form of installment loans is almost immaterial to your credit scores so don't focus too much energy or dollars on that type of debt. It's the credit card debt that's a problem, not your car loan or your mortgage or your student loans.”

Obviously, you want to stay current on all your loan obligations, but your credit card debt is most likely weighing down your credit score.

3. Use smart pay-down strategies

Paying down credit card debt doesn’t have to be a hassle or a chore if you adopt agood strategy. For example, one approach focuses on eliminating interest charges as quickly as possible and urges you to first pay down the credit card with the highest interest rate. You move onto the card with the next highest interest rate when that card is paid in full.

If you want to build a little payment momentum, you can focus your payments on the card with the smallest balance. Once this balance is paid in its entirety, you move on to the card with the next smallest balance.

“There are a variety of strategies on how to pay off or pay down credit card debt,” Ulzheimer says. “Some will help you pay down the most expensive debt first. Some will help you pay down the smallest debts first. Some will help you pay down the most score-damaging debts first. So, choose the method that fits best with your goals.”

Whatever strategy you choose, you’ll save money by knocking out high-interest credit card debt, and your credit score will get a lift.

“Reducing your credit card balances, if everything else is in good shape, could bump your (credit) scores up in just a month or two,” says Rod Griffin, senior director of public education and advocacy forExperian

4. Establish a new budget

A brand-new budget can help you combat overspending.

您将需要创建一个新的预算前进after overspending. Tally up your expenses and monthly bills, then calculate your total income. Are you working one 40-hour-a-week job or juggling two? Add together all your income, including side hustles. You want a clear view of just how much money you are making. What kinds of expenses can be cut? You are looking for money to pay down credit card debt and money to pay for essential items in your budget.

“Most people consider the word "budget" akin to a four-letter word as if the budget is going to take away all of their fun,” says Martin Lynch, director of education atCambridge Credit Counseling. “Instead, they should consider their spending plan as an effort to make sure they can reach their financial goals by eliminating or reducing their expenses for things that don't really matter to them.”

Getting your spending in line with your new budget will go a long way in creating a healthy financial outlook.

5. Tackle past due payments

If you’ve been a few days late or more on a credit account, you’ll want to take steps to pay that account in full. Doing so will help your credit and clear away the hefty penalty interest rates you may be paying.

“The most serious mistake consumers make that negatively impacts their credit score is late payments, so bringing those accounts current will help you get your credit moving in the right direction,” Griffin says.

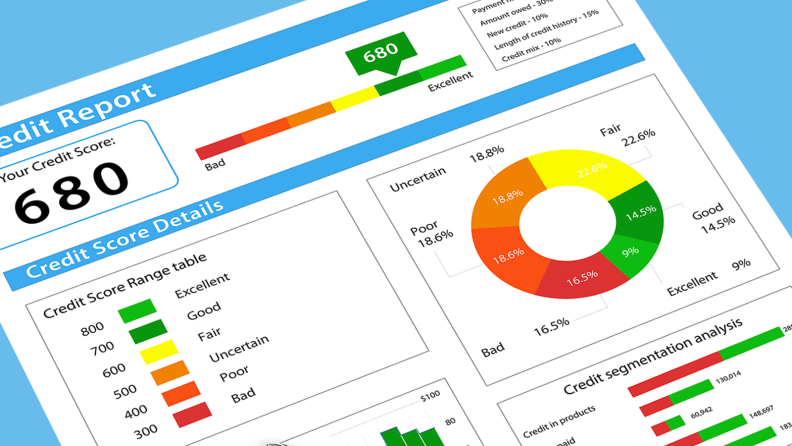

6. Check credit reports

Paying down credit card debt will improve your credit score.

To assess the status of all your credit accounts, you’ll want to get copies of yourcredit reportfrom the three national credit reporting agencies, Experian, Equifax, and TransUnion. VisitAnnual Credit Report.comfor free copies of your report.

In your credit report, you’ll find information on your credit accounts, including the type of account, such as a mortgage, car loan or credit card, your payment history on each account, and your credit limit or loan amount.

你想要一个精确的统计outstanding debts. How much do you owe? Is there an account with a small balance that you need to pay off? Taking care of a forgotten debt will boost your credit score.

“(Review) all three of your credit reports in an effort to make sure no debts are omitted,” Lynch says.

7. Keep accounts open

Once you look at all the accounts that are open on your credit report, you’ll want to leave them that way. When you keep a credit card account open, it will be counted in your revolving utilization ratio. Having an account with a zero balance and a hefty credit line will be good for your revolving utilization ratio, which will be good for your credit score.

Related content

The product experts atReviewedhave all your shopping needs covered. Follow Reviewed onFacebook,Twitter,Instagram,TikTok, orFlipboardfor the latest deals, product reviews, and more.

Prices were accurate at the time this article was published but may change over time.